Contract to Invoice to Payment (“Tinkers to Evers to Chance”) (Part II of II)

The SEC knows that it has powerful enforcement tools. The FCPA imposes two important requirements on issuers – keep accurate books and records and maintain internal controls to ensure that management’s accounting controls operate effectively to ensure proper use of corporate assets. The SEC knows these are broad requirements.

One critical area of focus has been the SEC’s focus on contract-invoice-payment process. For compliance professionals, this should be an area of high priority. Chief compliance officers have to work closely with procurement, payables, sales and other functions that touch these important procedures. CCOs have to work together to pull apart the process, understand the steps involved, and then build controls surrounding these activities.

Let’s take a quick look at some of the important issues:

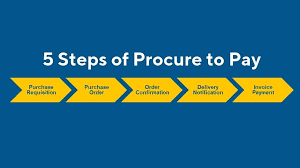

Contracting/Purchase Orders: Many companies fail to maintain contract management systems that can link contracts and purchase orders with the invoicing and payment process. Business contracts with third parties are particularly important because they set forth the schedule of payments, the specific goods or services to be provided, and invoicing requirements, including documentation, details and verification of goods and services. The contracts and purchase orders, at a minimum must include appropriate certification and compliance provisions depending on the risk associated with the transaction.

A contract/purchase order management system links together critical terms and conditions with invoice review and payment functions. This link is essential for an effective control environment. The absence of coordination among these processes is a recipe for breakdowns and illegal payments.

Companies have to apply these procedures to purchase orders because not all business transactions are conducted pursuant to a contract. It is essential to any set of financial activities that purchase order transactions are documented and coordinated with related and essential functions.

Invoicing: When paying third-party vendors, accounts payable staff are critical front line actors. Review of invoices can reveal unexplained charges, inflated fees and other means to release funds for improper purposes. Accounts payable personnel who have access to contract verification checks can make sure that payments are being made in accordance with contractual requirements, including documentation of goods and services provided, terms of payment, and appropriate charges.

Procurement plugs into these activities by onboarding new vendors and suppliers. Sales staff brings on new distributors and agents who create significant risks that require careful financial scrutiny over contracts, purchase orders and invoicing. As part of these functions, robust due diligence procedures are required to confirm ownership, legal compliance, reputation and other important issues needed to identify and mitigate risks.

Payment: Procurement, sales and financial operations closely coordinate on ensuring that payments are made in accordance with contractual/purchase order terms, that such payments are authorized for goods and services delivered, and that payments are made to the proper bank account or company.

Accounts payable bring together these important functions and serve as a critical check on the company’s controls. Accounts payable personnel are natural allies of compliance officers. Open communications and elevation of red flags by accounts payable to business and compliance functions should be authorized.

To ensure appropriate awareness, companies have designed and delivered robust compliance training for accounts payable staff to ensure familiarity with legal risks, including the FCPA, sanctions, money laundering and fraud. Account payable staff are eager to assist and embrace an active role in the compliance arena.

On the flip side of accounts payable, sales staff have to develop close working relationships with accounts receivable for collecting sales payments from distributors and agents. Again, these financial interactions raise bribery, money laundering (third-party payment) and fraud risks. Accounts receivable staff actively mitigate these risks and need similar access to review documentation and contract terms for accuracy.